Surge Group

AI Agents Becoming the First Native Users of Blockchain Finance

Others

A structural shift is emerging at the intersection of artificial intelligence, blockchain infrastructure, and digital payments. On May 7, 2026, Amazon Web Services, Coinbase, and Stripe announced infrastructure enabling AI agents to transact using USDC micropayments across blockchain rails via the x402 protocol. The development represents more than another crypto integration headline. It signals the early formation of an entirely new category of economic participant operating directly on digital financial infrastructure.

For the first time on a meaningful scale, autonomous software systems are beginning to interact with payment networks independently of human operators. These AI agents can hold wallets, receive payments, spend capital, purchase computational resources, and execute financial transactions without requiring traditional banking infrastructure or manual intervention. The AWS system specifically enables agents to pay for APIs, data feeds, paywalled content, and digital services in real time as they perform tasks.

That distinction matters because existing financial systems were designed around human identity. Banking infrastructure assumes account holders are individuals, corporations, or legally registered institutions. Compliance frameworks, onboarding procedures, payment approvals, and settlement systems all rely on human verification layers. An autonomous AI agent does not fit naturally within that architecture.

Blockchain infrastructure fundamentally changes those assumptions.

A wallet does not require citizenship, a passport, corporate registration documents, or banking approval in the same way traditional financial systems do. It requires only cryptographic access. That seemingly simple difference may become one of the most commercially significant characteristics of blockchain networks over the next decade as AI systems become increasingly capable of operating independently across digital environments. In March 2026, Changpeng Zhao stated that AI agents could eventually make one million times more payments than humans using crypto infrastructure. Whether or not that figure proves accurate, the broader directional trend is already becoming visible in live infrastructure deployments.

The emergence of AI-driven micropayments also exposes a structural weakness within traditional payment infrastructure. Existing financial rails were never built for autonomous, real-time, low-value transactions executed continuously by software agents.

Card networks and banking systems become economically unworkable when transaction sizes fall to fractions of a cent or when payment frequency scales into thousands of transactions per hour. Fee structures, settlement delays, geographic limitations, and compliance overhead make traditional systems poorly suited for the operational requirements of autonomous AI services.

Blockchain-based stablecoin infrastructure solves several of those limitations simultaneously.

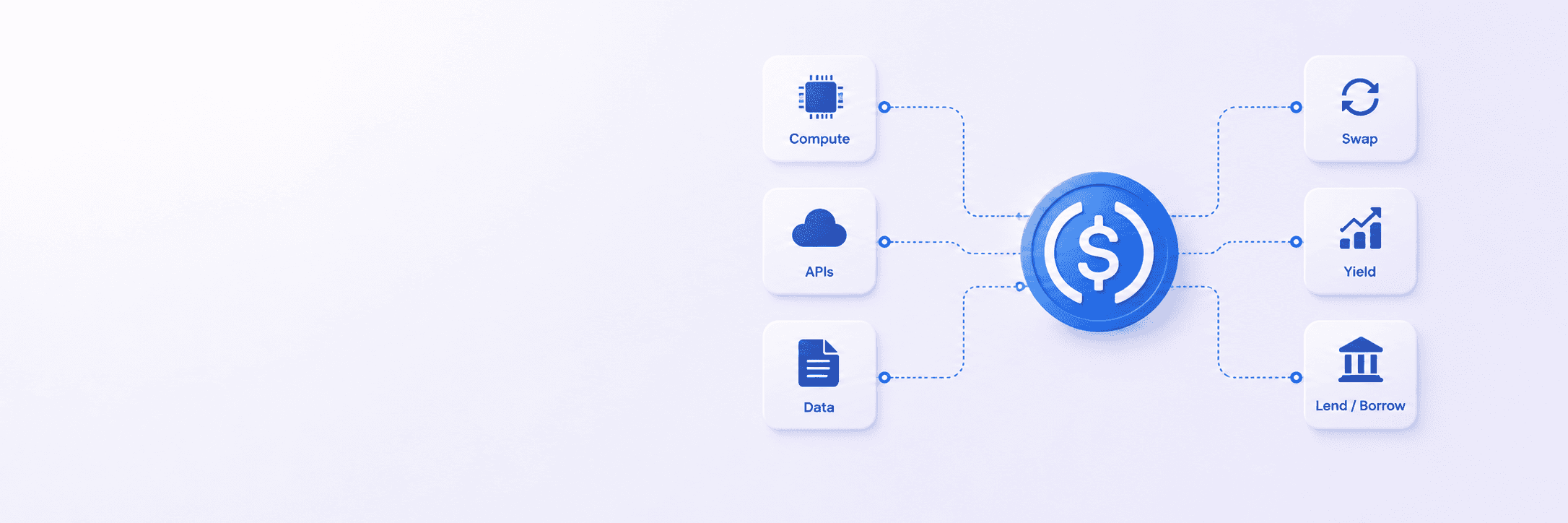

An AI agent can pay for compute resources minute-by-minute, purchase API access dynamically, compensate other agents for completed tasks, or monetise specialised services through continuous micropayment streams. Settlement occurs globally, twenty-four hours a day, without dependency on banking hours or intermediary approval chains. The use of USDC specifically reflects a growing institutional preference for stablecoin infrastructure as a programmable settlement layer. Stablecoins are being integrated into payment systems, treasury operations, remittance infrastructure, and cross-border settlement networks because they combine the mobility of blockchain rails with fiat-denominated price stability.

This creates an environment where AI agents are no longer limited to executing tasks. They can participate economically.

That shift changes how digital services may eventually operate. Instead of platform-based subscription models or centralised billing systems, future AI applications may transact continuously with one another across open financial rails. Services could become modular, composable, and dynamically priced in real time depending on demand, computation, or access requirements. The implications for financial infrastructure providers, cloud computing platforms, digital asset companies, and payment processors are substantial because the growth of autonomous economic systems introduces transaction categories that legacy banking infrastructure was simply not built to handle.

The broader significance of this development is that blockchain infrastructure appears increasingly aligned with the operational requirements of artificial intelligence in ways that may not have been fully anticipated when crypto networks were originally designed.

Decentralised finance infrastructure already allows users to lend, borrow, swap assets, generate yield, and access liquidity through programmable smart contracts. When those capabilities become accessible to autonomous software agents rather than only human participants, the nature of digital economic activity begins to change at a fundamental level.

An AI agent capable of generating revenue could theoretically allocate capital, rebalance holdings, pay operational expenses, source computational power, or interact with DeFi protocols autonomously depending on the permissions and parameters assigned to it. That introduces both substantial opportunity and serious risk.

Questions surrounding governance, liability, financial oversight, fraud prevention, and operational security will become increasingly urgent as autonomous agents begin interacting with live financial systems at scale. Regulatory frameworks across the US, EU, UAE, Singapore, and the UK are still adapting to stablecoins, tokenised finance, and decentralised infrastructure. The introduction of AI-driven economic actors adds a layer of complexity that regulators, institutions, and infrastructure providers will need to address within a compressed timeframe.

The commercial incentives, however, are already difficult to ignore.

The convergence between AI and blockchain infrastructure is generating new demand across stablecoin infrastructure, decentralised identity, smart contract security, AI payment orchestration, wallet infrastructure, compliance tooling, and autonomous financial systems engineering. Companies building in these areas are constructing the financial rails for machine-native commerce, a market that did not exist in meaningful form two years ago.

Over the next twelve months, the market conversation surrounding AI and crypto is likely to shift materially away from speculation and toward infrastructure deployment. The question is no longer whether blockchain networks can support programmable, autonomous economic coordination between machines operating globally. The infrastructure is already live. The remaining question is how quickly the rest of the financial system adapts around it.