Surge Group

Bitcoin ETF Are Revealing a Different Institutional Narrative

Others

Spot Bitcoin ETFs are beginning to expose one of the more important disconnects currently shaping digital asset markets. While public sentiment continues to oscillate between caution, fatigue, and recurring declarations that the cryptocurrency sector has entered another prolonged decline, institutional capital allocation data is telling a materially different story.

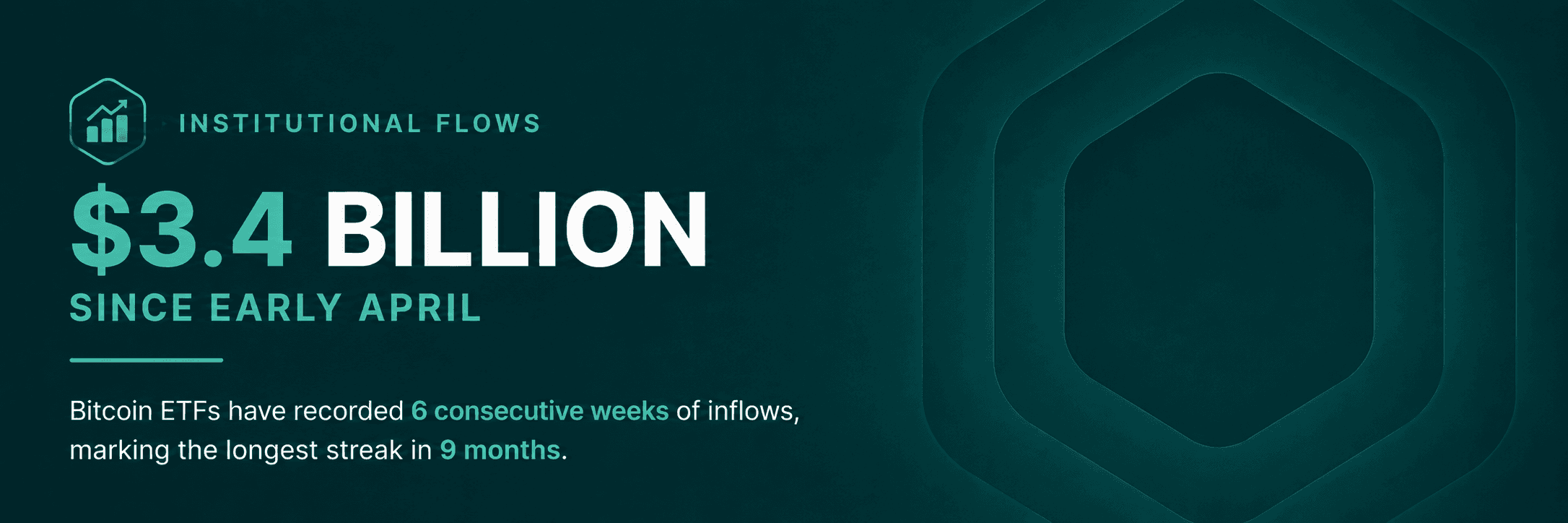

US spot Bitcoin ETFs have now recorded six consecutive weeks of net inflows, representing approximately $3.4 billion entering the market since early April 2026. BlackRock's iShares Bitcoin Trust (IBIT) led the streak's final week alone, capturing $596 million of a $622.75 million total weekly inflow across all Bitcoin ETF products. The streak marks the strongest sustained period of institutional accumulation in roughly nine months and arrives during a period where broader sentiment across retail markets remains subdued, with Bitcoin trading between $77,000 and $80,000 rather than at the speculative highs many anticipated following ETF approval.

That divergence between capital flow data and market narrative matters because it signals something structural rather than cyclical.

ETF flow activity consistently provides a more accurate reflection of institutional conviction than executive commentary, conference positioning, or public market statements. Capital deployment decisions inside pension funds, sovereign allocators, multi family offices, asset managers, and institutional wealth platforms are typically slower, more measured, and significantly more research driven than the short term sentiment cycles dominating online market discussions. When BlackRock’s IBIT continues attracting substantial daily inflows during periods of muted retail enthusiasm, it signals that institutional investors are increasingly viewing Bitcoin less as a speculative trading instrument and more as a long duration macro allocation tied to portfolio diversification, monetary uncertainty, liquidity positioning, and the evolving structure of digital financial infrastructure.

The current market environment presents a contradiction that many participants are struggling to interpret correctly.

Several crypto native firms continue implementing workforce reductions following the aggressive expansion cycles of earlier market phases. Coinbase reduced headcount by 14%, Gemini cut approximately 25% of staff, and venture deployment remains more selective than during the peak capital environment of 2021 and 2022. Trading activity across segments of the altcoin market has weakened considerably. Retail participation has not returned at the scale many expected following the approval of spot Bitcoin ETFs in the United States.

Yet institutional participation is expanding.

This distinction highlights an increasingly important structural separation emerging inside digital asset markets. Institutional investors are not allocating capital based on the same factors driving retail enthusiasm cycles. Their focus is tied to infrastructure maturity, regulatory clarity, custody improvements, liquidity accessibility, and Bitcoin’s positioning within broader macroeconomic portfolios.

For many institutional allocators, the investment thesis around Bitcoin in 2026 looks materially different from previous market cycles. The conversation has moved beyond speculative upside alone. Bitcoin is increasingly being evaluated alongside gold, sovereign debt exposure, inflation hedging strategies, and long term alternative asset allocations. The growth of regulated ETF products has significantly reduced the operational barriers that previously limited participation from large pools of traditional capital. Pension funds and institutional wealth managers no longer require direct custody infrastructure, exchange onboarding processes, or internal digital wallet management systems to gain exposure to Bitcoin.

That accessibility is changing the composition of capital entering the market.

ETF inflows tend to represent slower moving, structurally longer term capital compared to highly reactive retail flows. This type of allocation is less influenced by daily volatility and more influenced by long horizon portfolio construction decisions made across months rather than sessions. Sustained inflow periods carry broader implications for liquidity stability, market maturity, and long term institutional adoption trends that short term sentiment indicators consistently underweight.

One of the more important signals emerging from the current cycle is the widening gap between market narrative and capital flow reality.

Public sentiment remains cautious partly because many participants continue expecting institutional adoption to resemble previous speculative bull market behaviour. Instead, the current phase appears increasingly institutionalized, regulated, and infrastructure-driven. Capital is entering the market through traditional financial rails rather than through speculative retail expansion, and that transition is less visible, less dramatic, and consequently less covered.

Bitcoin trading near $80,000 without the retail mania of prior cycles may appear underwhelming to participants conditioned by previous market structures. Historically, however, periods where Bitcoin becomes less sensational and more structurally integrated into institutional portfolios tend to signal deeper market maturation rather than weakening relevance. The absence of headline-driven euphoria is not a signal of weakness. It may be a signal of normalization.

The broader implication extends beyond Bitcoin itself.

As institutional participation expands through ETFs, custody providers, regulated exchanges, treasury allocation strategies, and traditional wealth management platforms, the digital asset industry becomes increasingly interconnected with mainstream financial markets rather than operating as a separate speculative ecosystem. That interconnection has direct implications across recruitment demand, compliance infrastructure, regulatory development, capital formation, and product strategy throughout the sector. The roles being filled in Dubai, London, New York, and Singapore today are not being filled in anticipation of another retail cycle. They are being filled in anticipation of a structurally different market.

The firms, investors, and operators paying attention to institutional flow data rather than short-term sentiment cycles are better positioned to understand where the digital asset market is heading next.

In financial markets, capital allocation decisions reveal conviction long before public narratives catch up. The six-week Bitcoin ETF inflow streak is one of those signals. The question is how many market participants are paying attention to it.